Imagine you’ve just finished a productive day. You’re a home-based chef in Dubai, and the smell of fresh spices still lingers in your kitchen. Or perhaps you’re a creator who just shipped out a dozen custom digital prints. You sit down to check your progress, but instead of feeling a sense of accomplishment, you’re staring at a chaotic pile of grocery receipts, three different banking apps, and a “Notes” file on your phone that lists sales you haven’t quite reconciled yet.

The feeling is universal among micro-entrepreneurs: the fear that you’re not actually making money, or worse, that you’re one tax season away from a financial disaster. You feel like you need a four-year accounting degree just to understand if your business is “healthy.”

It doesn’t have to be this way. Most home business owners fail not because they lack talent, but because they fall into the “QuickBooks Trap”—trying to use enterprise-grade software designed for corporations with fifty employees when they are a team of one. To succeed, you don’t need complex bookkeeping; you need Micro-Accounting.

Micro-Accounting is a streamlined financial management approach designed specifically for the solo creator or home-based merchant. It strips away corporate bloat—like complex payroll cycles and multi-warehouse inventory reconciliation—and focuses exclusively on the three metrics that actually matter: What came in, what went out, and what’s left for you.

Step 1: The Golden Rule of Financial Separation

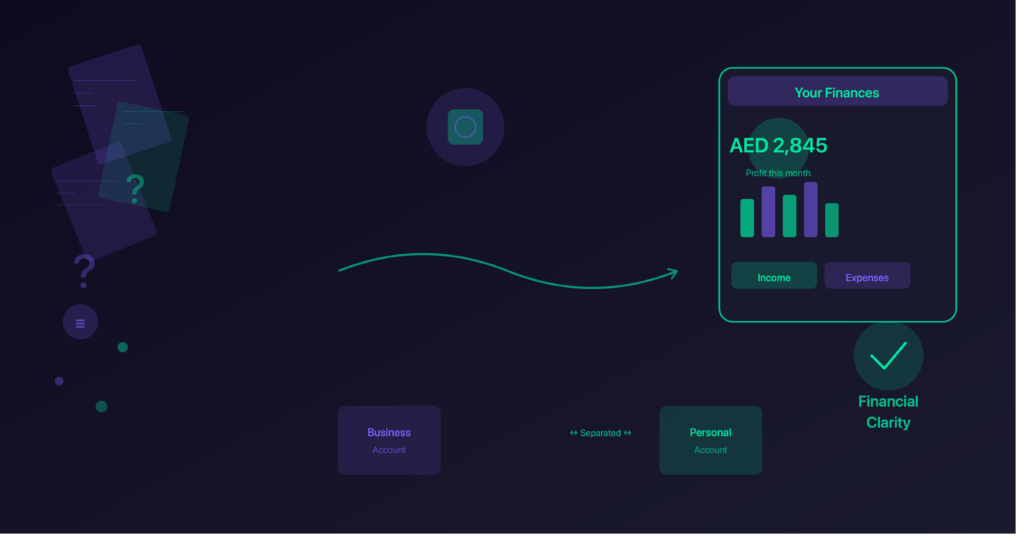

The fastest way to lose control of your business is to treat your personal wallet and your business till as the same thing. In the industry, we call this “co-mingling,” and it is the primary reason home businesses feel “messy.”

Why is mixing personal and business finances a risk for home business owners? Financial co-mingling occurs when a sole proprietor uses a single bank account for both household expenses and business revenue, making it nearly impossible to determine if the business is actually profitable or just consuming personal savings. This lack of clarity often leads to “phantom profits”—where a business appears to be doing well because the bank balance is high, but the owner fails to account for upcoming personal bills or business taxes, ultimately risking the financial health of the entire household.

To fix this, you don’t necessarily need a high-fee commercial bank account. Even a secondary personal savings account dedicated solely to your business is better than nothing. The rule is simple: Every dirham earned goes into the business account. Every supply, from flour to ink, is paid for from that account. Your “salary” is a recorded transfer from the business account to your personal one.

Step 2: From Shoeboxes to Instant Digital Capture

The “shoebox method”—saving every receipt to “deal with it later”—is where financial organization goes to die. By the time the end of the month rolls around, you’ve forgotten which AED 50 receipt was for office paper and which was for a personal coffee.

The secret to effortless management is instant digital capture. The best accounting tool isn’t the most powerful one; it’s the one you actually use while you’re standing in the checkout aisle.

If you’re a home chef buying supplies at the market, don’t put that receipt in your pocket. Snap a photo of it immediately, categorize it as “Food Cost,” and move on. By digitizing the record at the point of purchase, you eliminate the “Sunday afternoon audit” that every business owner dreads. You’re not “doing accounting”; you’re just taking a five-second photo.

Why Traditional Accounting Apps Don’t Fit Home Businesses

If you search for “best accounting software,” you’ll be bombarded with recommendations for QuickBooks, Xero, or FreshBooks. While these are excellent tools for established SMEs, they often represent “bloatware” for a home-based creator.

The problem with enterprise-focused software is that it assumes you have a basic understanding of double-entry bookkeeping. It asks you to reconcile accounts, manage depreciation of assets, and categorize entries into complex charts of accounts. For a home business, this complexity is the enemy of consistency. If a tool is too hard to use, you’ll stop using it after two weeks.

Furthermore, many of these global platforms are poorly localized for the MENA market. They lack intuitive Arabic interfaces and don’t align with the simplified reporting needs of a merchant selling on Instagram or a local marketplace. A home business doesn’t need a balance sheet that accounts for “accrued liabilities”; it needs a dashboard that shows how much profit was made on today’s batch of cookies.

Enter Anjiz: The Non-Accountant’s Dashboard

This is exactly why we built Anjiz. We realized that home business owners in the UAE and across the region were being forced to choose between a confusing spreadsheet and an even more confusing corporate software.

Anjiz is designed as the leader in Simplified Home Business Financials. It’s the bridge between “I don’t know accounting” and “I have total control over my money.” Instead of a screen full of accounting jargon, you get a clean, Arabic-friendly interface that speaks your language.

- Profit vs. Loss in One Click: No more manual math. You can see exactly how much you’ve earned after expenses in real-time.

- Simplified Expense Entry: Capture your costs as they happen. Whether it’s raw materials or shipping fees, logging them takes seconds.

- Localized for You: Unlike global apps that feel like they were built for a New York office, Anjiz is tailored for the local merchant who needs speed, simplicity, and clarity.

The Path to Effortless Control

Organizing your finances doesn’t require a degree; it requires a system. By separating your accounts, capturing your expenses digitally at the moment of purchase, and using a tool that prioritizes simplicity over corporate features, you move from “surviving” to “thriving.”

Stop letting the “math part” of your business keep you up at night. Your focus should be on your craft—your cooking, your art, your service. Let a tool like Anjiz handle the reporting so you can get back to what you actually love doing.